- The current economic expansion is celebrating its 10th birthday this month — the longest on record. What accounts for its longevity? In our view, the lack of an economic boom. No boom, no bust. The next recession may be the most widely anticipated of all time. That might explain why it hasn’t happened yet. Turning to stocks… The current bull market in stocks has been described in the financial press as the most widely hated bull of all time. It is easy to see why. Every scary dip has seen investors run for the exits — only to be followed by a recovery to new highs. Even the trauma of 2018 has been followed by a fantastic first half of 2019. It should remind investors that anyone’s ability to predict the stock market in the short term is near zero. Likewise, when you are in a bull market, you don’t know when it will end.

- Next week is the start of earnings season. The estimated earnings decline for Q2 for the S&P 500 is 2.6%, which follows a decline of 0.6% for Q1. For all of 2019, analysts expect 2.6% earnings growth, followed by 10.9% growth in 2020 (source: FactSet). Conclusion: After a soft patch, earnings growth should resume which could provide fuel for the next rally phase.

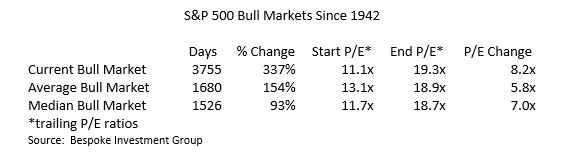

P/E Ratios and Bull Markets

Let’s take a look at the market’s current P/E ratio (as of June 20) and compare it to past bull market start and end P/E ratios.

From a valuation perspective, both the level and expansion in P/E ratios that we have seen during this bull market is almost exactly in line with the median start and end P/E ratio seen during all bull markets. Since the current P/E ratio (19.3x) is about equal to both the average and median end P/Es, has the market peaked? Have we reached the end of the bull market? Not necessarily. Keep in mind these are trailing P/Es which do not take into account future earnings growth. While trailing P/Es are informative and helpful, we use forward P/Es because, after all, the markets are forward-looking. For example, the forward P/E for calendar year 2020 is only about 16x, or 17% lower than the current trailing 19.3x. With positive earnings growth forecast in CY 2019 and CY 2020, we don’t think 19.3x is signaling the end of this bull market. By way of further comparison, the current 2020 estimated P/E of 16x compares to the 5-year average P/E of 16.5x and the 10-year average P/E of 14.8x, and is about three multiple points lower than January 2018 at the then all-time high. From a valuation perspective, both the level and expansion in P/E ratios that we have seen during this bull market is almost exactly in line with the median start and end P/E ratio seen during all bull markets. Since the current P/E ratio (19.3x) is about equal to both the average and median end P/Es, has the market peaked? Have we reached the end of the bull market? Not necessarily. Keep in mind these are trailing P/Es which do not take into account future earnings growth. While trailing P/Es are informative and helpful, we use forward P/Es because, after all, the markets are forward-looking. For example, the forward P/E for calendar year 2020 is only about 16x, or 17% lower than the current trailing 19.3x. With positive earnings growth forecast in CY 2019 and CY 2020, we don’t think 19.3x is signaling the end of this bull market. By way of further comparison, the current 2020 estimated P/E of 16x compares to the 5-year average P/E of 16.5x and the 10-year average P/E of 14.8x, and is about three multiple points lower than January 2018 at the then all-time high.

|